info@meradia.com

info@meradia.com

SUMMARY

Environmental, Social and Governance (ESG) investment strategies and other portfolio management strategies that accentuate societal impact into the investment management process are burgeoning in popularity. Changing attitudes and demographics suggest that clients are increasingly interested in using their investment dollars to make positive impacts.

These new impact strategies challenge traditional investment performance reporting. This article examines the core characteristics of impact investing, barriers to improved performance reporting and tools to navigate this changing landscape.

INTRODUCTION

Environmental, Social and Governance (ESG) investment strategies incorporate social impact objectives into the investment management process. Social impact goals and the portfolio’s impact aspirations vary widely, from addressing important global issues such as climate change (Environmental), fair labor policies (Social), and executive compensation (Governance). They may even include goals affecting individual communities. The popularity of ESG investments has risen sharply as firms commit more resources to meet the increasing needs of a diverse investment clientele who are interested in using their investments to make positive impacts.

With this growing investment class comes a need to reevaluate performance reporting considerations since ESG investments have more nuanced performance or client reporting needs than traditional alpha-seeking strategies. Investment Performance professionals attempt to show performance and analytical measures that demonstrate how well Portfolio Managers perform relative to stated investment objectives. Delving into the social impact sphere challenges traditional investment performance concepts. Investment performance professionals are challenged to quantify impact and create transparency to the social considerations influencing the investment decision process. For a profession firmly rooted in the objectively quantifiable, delving into subjective impact reporting will require re-tooling.

SOCIAL IMPACT INVESTING SPECTRUM

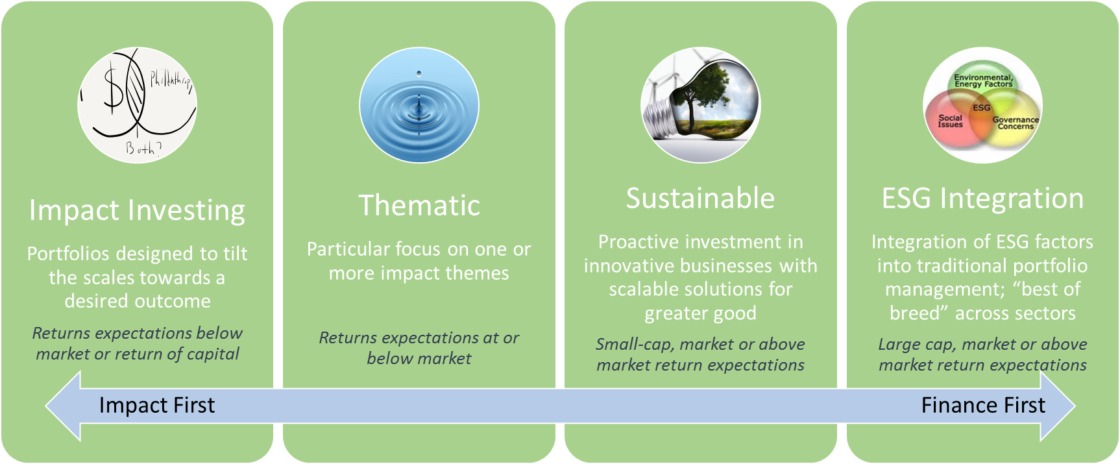

There are different options for investors across the social impact investing spectrum. Understanding the various types of investment objectives is important when evaluating the tools and data available to include in client-facing performance reports. The categories below broadly describe the social impact investing continuum in the marketplace today.

Impact Investing strategies, also called “Impact First,” focus on achieving or tilting the balance towards a specific, intentional outcome. Typical asset types include direct loans, impact bonds, community financing deals, and micro-finance start-ups. Impact strategies focus on impact, not financial returns, first. They expect little to no performance returns, focusing on a return of capital. They eschew traditional alpha for the desired change. Impact-first investors may not even choose a benchmark for their investment since there may not be one that would suffice for their goal, such as improving employment opportunities for low-income neighborhoods in struggling cities. Demonstrating if the desired impact was achieved is a challenge for performance professionals. Impact investing can be an attractive alternative to philanthropic giving as impact investing comes with the expectation of the return of capital invested. A different tool than philanthropic giving, impact investing is used to encourage capitalistic approaches to solve societal problems. Returns are expected to be zero at best and are often negative. Unsurprising, charitable endowments and foundations are large investors and leading industry efforts to understand and quantify social impact. (i)

Thematic Investing strategies focus on one or more global themes such as clean water, advancement of women and girls, deforestation or perhaps reducing poverty in a specific geographic location like Africa. Thematic investing tends to have returns expectations at or below market, indicating the strong focus on achieving results supporting their specific global theme. As with Impact Investing, the performance reporting challenge is how to show impact relative to stated investment objectives. For example, if the theme relates to improving access to clean water, the performance report should demonstrate how the investments within the portfolio support this social agenda.

Sustainable Investing strategies make proactive investments in companies with scalable solutions that benefit the greater good. Many of these are small and mid-cap companies, including innovative technology firms like Tesla. Portfolio Managers touting sustainable investing strategies might look at US mid-cap firms and select the top 50 when viewed from a sustainable technology perspective. At this spot in the social impact continuum, investors are more concerned about investment returns. They may indeed be choosing sustainable technology investments precisely because of perceived long-term value. Investment performance reports therefore need to consider traditional measures alongside impact measures. A relevant comparison may be comparing a sustainable strategy to a comparable mid-cap index that doesn’t incorporate this impact lens.

ESG Integration investments most resemble traditional investments. They are sometimes referred to as “Finance First.” ESG Integration investors do care about performance returns and often have higher return expectations. Industry experts argue that good corporate practices correlate to greater corporate earnings as they mitigate risks that result in significant corporate losses. Portfolio managers find these “good corporate citizens” in the large cap space by analyzing numerous factors, metrics and research to include firms with attractive scores across a wide variety of Environmental, Social or Governance characteristics. Strategies in this category tend to focus on best-of-breed companies who score higher on ESG screenings than their peers. Asset Managers employ a variety of data providers, such as Sustainalytics, Bloomberg ESG and MSCI, for ESG factor inputs as consistency across data providers can vary widely. (ii)

To create visibility about decisions to include investments, performance reports should include the screening criteria used alongside traditional performance measures and existing benchmarks. This complex web of inputs challenges performance reporting since adherence to market data contracts often prohibits a blatant combination of provider inputs on external client reports.

BY THE NUMBERS: ESG INVESTING

Social impact investing has grown by leaps and bounds and shows no sign of slowing. A strengthening focus on responsible investing attracts more investors and assets every year.

Global AUM for social impact investing has surpassed $500 billion according to Global Impact Investing Network (GIIN) in its paper “Sizing the Impact Investment Market.” (iii) The rise in popularity of ESG strategies is directly linked to investors’ growing preference to use their investments to help change the world for the better. Many investors believe that good corporate citizens make for good investment choices. This phenomenon has raised considerable red flags across the industry as regulators struggle to make sense of how best to ensure that investment goals were achieved when those goals are subjective.

PERFORMANCE RETURNS FOR IMPACT STRATEGIES

It is still too early to accurately and repeatably calculate social impact returns. Most data ESG is self-reported by companies and inconsistent, while the variety of ESG measures are too numerous to effectively leverage in analysis. Social impact measures are riddled with subjective and contradicting inputs (iv) and continue to present the largest challenge to performance reporting. Attempting to reduce inherent ambiguity, regulatory bodies and corporate auditors are actively working to drive consensus and standardization. Watch for rapid evolution if standardization efforts prove fruitful.

With respect to performance of ESG Integration strategies, which constitute the largest percentage of social impact investments, two perspectives emerge. Some believe considering ESG factors adds to risk-adjusted return, thereby improving performance. That is, companies with good environmental, social and governance practices offer better long-term investment potential. The counter view is that ESG strategies detract from returns or their impact is inconclusive. Underpinning this view is the strong negative correlation that ESG strategies have with the fossil fuel market due to their environmental bent. If oil prices tick upward, then ESG performance is likely to suffer relative to the larger market.

Does the immaturity of impact data or the correlation of ESG to fossil fuels matter to an investment performance professional? One mission of performance reporting is to present factors influencing the investment process; and thereby improve transparency. The question is how best to improve transparency to the underlying factors involved in impact or ESG portfolio decision making.

During the past decade, performance operations have been pushed to focus on data quality and process efficiency. In doing, all portfolios are viewed the same way, or through a few different lenses. Bespoke reporting to illuminate nuances about a portfolio strategy has fallen by the wayside to investors’ detriment. While the focus of performance professionals continues to be the accuracy of results, they should also be considering answering this and other investor questions. Competition is generally moving the pendulum back towards bespoke, strategy-specific performance reporting. This is particularly true for social impact strategies as investors crave regular reinforcement of the ideals that shaped their investment choice.

PERFORMANCE REPORTING CONSIDERATIONS

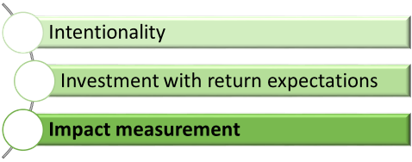

According to the Global Impact Investing Network (GIIN), three factors define impact investments: intention (do something good), stated returns expectations (even if none) and measurability (the ability to assess intended impact). Measuring performance of ESG investments centers on analyzing the intended impact of the strategy, so performance tools should vary to effectively measure the impact achieved.

When it comes to impact investing, performance reporting is lacking. Impact investing has unique aspects that require deeper analysis than what is typically found on performance reports. In reviewing hundreds of performance reports for ESG strategies, typical data points emerged: Performance Returns (1y, 3y, 5y), Top Holdings, Country Weights, GICS Sectors and basic characteristics like market cap or standard deviation. Searching for good examples of best practices related to impact investment performance reporting proved fruitless. Little or no data is apparent to directly support the social impact inspired investment thesis.

Interestingly, data does exist and can be found in other industry material, specifically in client pitch decks. Sales materials leverage these inputs to justify the investment thesis. By using and including available data, performance measurement professionals can provide clients with performance reports that show:

- Impact factors influencing the investment decision-making process

- Rationale for each choice relative to the intended impact

- Which securities were included and why

Portfolio managers understand the limitations of performance reports and factsheets to display ESG details and, as a result, often use customized pitch decks to provide clients with additional ESG details. In effect, managers pitch ESG strategies to clients without having the ability to effectively measure the impact of these strategies once the client has invested.

Impact investments challenge the one-size-fits-all approach to performance measurement. To capture the performance of an ESG investment, impact factors merit inclusion in performance reports.

BARRIERS TO IMPROVING IMPACT PERFORMANCE REPORTING

While the need for improved performance measurement reporting for impact investments is obvious, implementing the necessary changes is a significant undertaking. The change in perspective – measuring impact instead of pure returns – represents a paradigm shift for investment performance specialists in providing meaningful performance reporting. To provide greater transparency and detail with respect to impact investments, firms will need to overcome several key obstacles.

- Convention – Many firms have the mindset of “this is how we do it.” As ESG strategies continue to attract investors, and especially as wealth transfers from older generations to younger ones, firms will need to adapt to meet client demand. With respect to performance reporting, firms will need to include relevant impact details and criteria to help clients understand how their ESG strategies are performing (i.e., affecting change). Firms that don’t adapt run the risk of being left behind as the industry transforms to meet new performance reporting best practices.

- Standards – GIPS standards govern traditional performance measurement reporting; however, no such standards yet exist for measuring ESG claims. Firms interpret ESG factors in different ways. The resulting discrepancies can undermine the perception of accuracy. Since investment performance professionals depend on high quality data to produce accurate performance reports, a lack of data quality leads to a lack of confidence in the validity of the results. Best practice standards are evolving to provide performance measurement staff with guidance. (The CFA Institute is actively developing standards for ESG-related disclosures and are accepting comments through October 2020.) (v) Having comparable standards promotes transparency, and investors like the comfort of familiar, known and easily understandable information.

- Input Immaturity – With a short track record relative to other investment products, ESG strategies have immature inputs. Even so, the popularity of impact investing compels firms and investment professionals to adapt processes and may include various sources of ESG factors in portfolio inclusion criteria. Despite the relative newness of inputs and data, performance teams can leverage internally developed methodologies to slice and dice returns.

- Systems Investment – Infrastructure changes present the most imposing challenge for the industry to overcome in producing better performance reporting supporting impact investments. Implementing change is difficult, requiring an investment in time, resources, systems and functionality. Introducing functionality to capture data and measure performance for impact investments requires changes in data structures, systems, calculations, and processes. For the performance professional, it also requires additional training to understand the unique factors influencing performance of impact investments, i.e., how to factor in subjective criteria.

ESG PERFORMANCE, FACTORS & RATINGS

Performance measurement specialists understand that traditional performance reporting includes the following components: returns, benchmarks, classifications, characteristics and style. For ESG strategies an additional four unique components are required.

1. ESG Issuer-Level Factors

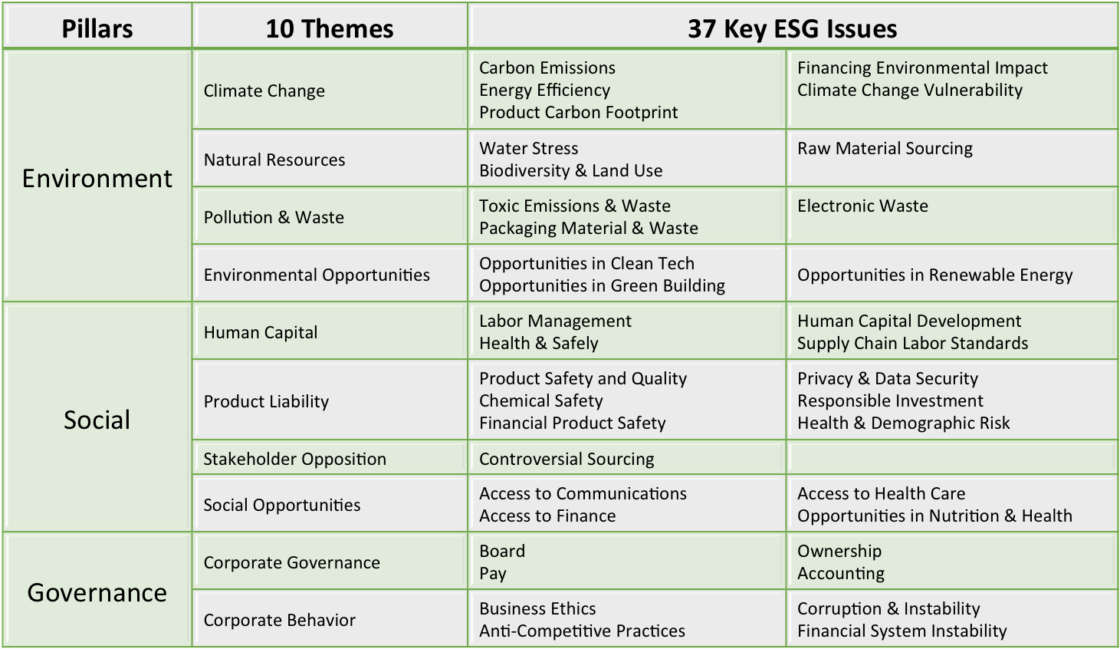

Portfolio managers consider many criteria when analyzing companies for potential investment. For impact investments, these also include various environmental, social and governance factors. Many data providers offer security-level data inputs, which are designed to quantify risk and other attributes. MSCI has an extensive ESG ratings methodology covering each of the three ESG pillars, the themes within each pillar, and the key issues within each theme. Note: many vendors play in this space, uniquely rating securities against their own ESG framework.

The following chart includes the key performance indicators tracked by MSCI.

Source: MSCI ESG Ratings Methodology

Portfolio managers often combine their own independent research with multiple ratings sources. The resulting internal ratings could be leveraged by performance teams like bond ratings.

2. ESG Fund Ratings

An alternative to security ratings, several data providers rate funds relative to internally developed ESG rankings. Morningstar places emphasis on financial factors as opposed to impact. Morningstar uses security-level data from Sustainalytics to calculate overall portfolio scores such as ESG Score, Controversy Score and Sustainability Score. GIIRS, which uses B-Analytics security-level data, look to identify an investment’s impact. B-Analytics attempts to extrapolate impact measurement by guiding companies through an extensive questionnaire. GIIRS gathers individual company ratings and calculates an overall fund score.

Fund rating providers produce data useful to performance measurement professionals in creating meaningful performance reports. ESG fund scores and ratings are key components of the investment decision-making process and can be included on performance reports. Displaying ratings and fund scores for impact investments are a good start to showing investors portfolio level characteristics. A challenge for performance specialists is the reliability of ratings. When the ratings are based on information a company discloses, particularly non-financial information, the result is subjective so firms should consider including sources and uses of ESG factors in footnotes and disclosures.

3. Classification

Classifying performance returns into GICS structures helps investors understand the industry and sector bets inherent in a given portfolio strategy. This structure; however, was intended to be generic and therefore lacks nuances associated with impact investing. Impact investments delve into social spheres or environmental categorization GICS was never intended to make clear. The Sustainability Accounting Standards Board (SASB) was launched to develop a framework, standards and best practices relative to impact investments. SASB has a focus on the disclosure of non-financial attributes. The organization has widespread and key participant support, as the need for better disclosure and reporting is universally acknowledged. Without it, performance reporting specialists will struggle to develop best practices supporting impact investments.

The Sustainability Industry Classification Schema (SICS) is an offshoot of SASB. Like GICS, SICS categorizes firms into industry and sectors. It differs from GICS in that it also offers sub sectors supporting impact investments, including alternative energy, biofuels, solar energy and wind energy.

The investment industry would be well served to move beyond the traditional GICS schema when it doesn’t serve the need for investors. Incorporating a new schema like SICS would be relatively easy as its constructs mirror the hierarchical, security master-based structures inherent in other supported schemas. The SICS classification could provide investment performance professionals with greater accuracy and transparency in truly assessing performance of impact investments. This is not unlike the variety of sector schemas available in the Fixed Income space, such as Municipals, High Yield or Investment Grade products. The bottom line on classification: moving away from GICS can greatly enhance transparency for impact investments.

4. Impact Style Analysis

Style analysis is an important tool to compare funds to benchmarks and peers. Style tools have evolved to leverage ESG ratings inputs to compare funds’ according to ESG category scores. Continue to view these new style metrics with caution as they depend on underlying scoring, which is still based on subjective, inconsistent self-reporting as mentioned previously. Until these reporting metrics can be standardized the resulting comparisons can be confusing at best and misleading at worst.

5. Benchmarks

Initially, impact strategies used generic benchmarks, such as the S&P 500 index. New benchmarks are rapidly emerging to improve relative analysis and to meet growing demand for passive ESG and ETF investment options. Traditional benchmark vendors boast thousands of ESG and thematic impact indexes while newer vendors are emerging to fill specific needs. Performance Operations may be asked to manage new sources for benchmark comparators.

CONCLUSION

Performance measurement professionals face an increasing challenge from impact investments in evaluating performance and creating reports that provide investors with an accurate depiction of impact investment performance. At the same time, tight scrutiny is needed due to the immaturity of inputs. New standards are quickly emerging. Attributes supporting security-level analysis (ESG factors) will improve, and this will enhance the quality of performance measurement. Firms must evaluate portfolio-level ESG impact scores and push for alternative industry classifications to improve sector visibility. Fast-growing demand for ESG strategies will improve data quality, transparency and reporting for performance measurement professionals tasked with evaluating and reporting on impact investing performance.

HOW MERADIA CAN HELP

Meradia has proven methodology and skills to help asset managers improve their performance reporting and the data that supports it:

- Performance, risk and analytics

- Information delivery and reporting

- Process design and change

ENDNOTES

i Addy, C., Chorengel, M., Collins, M & Etzel, M. “Calculating the Value of Impact Investing.” Harvard Business Review (January-February 2019): 102-109. https://hbr.org/2019/01/calculating-the-value-of-impact-investing

ii Kumar, Rakhi & Weiner, Ali. “The ESG Data Challenge.” SSgA Article (March 2019) https://www.ssga.com/investment-topics/environmental-social-governance/2019/03/esg-data-challenge.pdf

iii Mudaliar, Abhilash & Dithrich, Hannah. “Sizing the Impact Investing Market.” GIIN Publication April 1, 2019: 1 https://thegiin.org/research/publication/impinv-market-size#:~:text=The%20GIIN%20estimates%20the%20current,of%20the%20impact%20investing%20market.

iv Kotsantonis, Sakis, and George Serafeim. “Four Things No One Will Tell You About ESG Data.” Journal of Applied Corporate Finance 31, no. 2 (Spring 2019): 50–58.

v “Consultation Paper on the Development of The CFA Institute ESG Disclosure Standards for Investment Products”, (August 2020) https://www.cfainstitute.org/en/ethics-standards/codes/esg-standards

ADDENDUM

Laurie is among The Spaulding Group’s The Journal of Performance Measurement® 2020 Dietz Award Winners for this paper.